Coverage of classic and exotic vehicles prioritizes insurance policies designed for collectible, rare, or uniquely valuable automobiles. These arrangements often differ from standard vehicle insurance because they reflect the distinctive risks, value assessments, and preservation standards associated with classic, vintage, and luxury vehicles. Instead of referencing only market value, these policies may use agreed value or stated value methods to clarify the insured amount. Protection typically considers limited usage, security measures, and preservation status.

Classic and exotic car insurance often includes features that account for restoration work, the original condition of the vehicle, and limited annual mileage. Owners may benefit from tailored risk-management techniques such as secure storage requirements, approved appraisals, and specialized repair or parts provisions. Many policies also set forth eligibility criteria regarding age, rarity, or custom modifications of the insured vehicle. Overall, these forms of insurance reflect the specialized needs of collectors and enthusiasts.

Policies tailored for classic and exotic cars rely on careful valuation methods. Most plans offer agreed value, where the vehicle’s worth is determined upfront through appraisals or documented restoration investments. This process differs from actual cash value policies that are more common with standard auto insurance. Agreed value can help protect vehicle owners from depreciation in the event of total loss, subject to policy terms and conditions.

Limited usage and secure storage are often important in eligibility for classic and exotic car insurance in the United States. Insurers may ask for evidence of storage in a private garage or secure facility. These measures can help reduce risk and may lead to different premium calculations. In addition, policyholders are frequently required to demonstrate proof of another primary vehicle if the insured car is not intended for daily transportation.

Specialized policies often cover both accidental and non-accidental risks, such as theft, vandalism, natural disasters, and transport hazards. Many insurance providers in the United States also offer optional extras, such as coverage for spare parts or endorsement for show and exhibition usage. These specialized provisions can be a factor in establishing premium levels and are usually clearly described in policy documentation.

Eligibility rules in dedicated classic and exotic car coverage commonly specify minimum vehicle ages, restoration standards, or even maximum annual mileage. Vehicles that have undergone significant modifications may be assessed differently than those in original condition. Policyholders are generally asked to provide photographs, appraisals, or documentation to support accurate risk assessment and valuation.

Comprehensive coverage for rare or collectible vehicles plays a specific role in the automotive insurance landscape. By considering appraisal values and owner usage patterns, these policies aim to address situations not covered by standard insurance. The following sections focus on specific components of classic and exotic car insurance, including detailed looks at policy features, costs, valuation, and owner considerations.

One of the prominent characteristics of insurance for classic and exotic vehicles in the United States is the use of agreed value coverage. This strategy establishes a vehicle’s worth through documentation and mutual consent between the owner and insurer, instead of relying on market depreciation. Owners may submit restoration records, purchase receipts, or appraisal reports for underwriting. In the event of a covered total loss, the pre-determined value may serve as the basis for claim settlement, subject to policy conditions.

Usage limitations distinguish classic and exotic car policies from more traditional auto insurance plans. Many providers specify annual mileage caps, often between 1,000 and 7,500 miles per year. This helps define the vehicle as a collectible rather than a daily-use car. These restrictions, along with use requirements that favor participation in events or exhibitions, can influence the overall cost and structure of coverage.

Classic and exotic car policies often include specialized parts and labor coverage. Since repairs may require rare or imported components, insurers may allow higher expense limits for finding or shipping these items. Policies might also grant flexibility in choosing repair shops with expertise in collector vehicles, rather than requiring use of standard network providers. This type of flexibility is usually specified in the policy language.

Optional add-ons are common in this category of insurance. These might include spare parts coverage, coverage for automobilia, or protection during transport to shows and auctions. Owners may select these features according to anticipated use or potential risk exposures. Cost implications and eligibility for these extras are generally included in detailed policy disclosures from United States-based insurers.

The calculation of premiums for classic and exotic car insurance in the United States relies on variables such as vehicle age, condition, storage situation, and usage reports. Premiums may start below $300 annually for less valuable collector cars stored in secure conditions, and rise into the thousands for rare or high-value exotics. Documentation supporting agreed value or restoration investments typically forms part of the risk and pricing assessment.

Insurance providers may require regular vehicle appraisals to confirm value over time, especially for vehicles that are actively restored or rise in market demand. In some cases, owners may choose to update agreed value at policy renewal to reflect upgrades or changing market conditions. Participation in car clubs and annual collector events can also sometimes be used as supporting evidence for risk management and valuation purposes, as referenced by insurers such as Hagerty and Grundy.

Storage plays a key role in cost determination. Vehicles kept in climate-controlled or highly secure facilities typically present less risk and may see more favorable premiums. On the other hand, collectible vehicles kept outside or used frequently may carry higher associated costs. Insurers usually perform verification through owner-provided photographs or inspections before confirming these details in policy agreements.

Mileage restrictions, event participation, and intended vehicle use may impact both policy eligibility and premium costs. Insurers may require that a classic or exotic vehicle not serve as a primary means of transportation and typically ask for another primary-use vehicle to be listed on the policy. Non-qualifying usage or exceeding mileage allowances could influence annual costs or policy terms, according to most United States-based collector car insurance documentation.

Eligibility for classic and exotic car insurance in the United States typically involves age parameters. Many policies reference a minimum vehicle age, such as 25 years, although newer exotic or limited-production vehicles may qualify if deemed collectible through specific underwriting guidelines. Insurers often request details regarding modifications, restoration status, and historical value in the application process.

Occupational standing, driving history, and the presence of a separate daily-use vehicle can influence underwriting decisions. For example, an applicant with recent major driving violations or an absence of a primary-use car may encounter restrictions or additional requirements. Many insurers in this sector ask for clean driving records and limited annual mileage to mitigate risk and remain consistent with collector use.

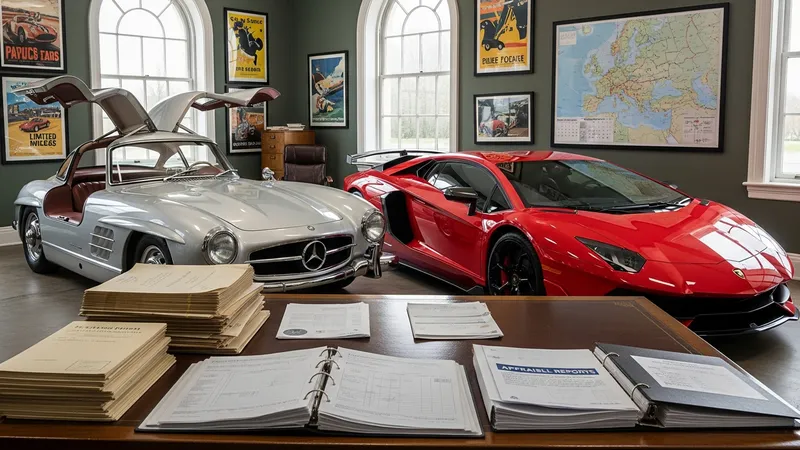

United States-based collectors may be required to provide detailed photographs or take part in certified appraisals before coverage is issued. Documentation confirming restoration or originality, as well as secure storage arrangements, can be necessary for policy acceptance. These processes allow underwriters to assess each vehicle’s individual risk and establish terms that reflect the unique nature of collectible or high-value cars.

Vehicle use outside the context of the owner’s household or participation in rideshare programs is typically restricted by most collector car policies. Insurers usually note these limitations during initial underwriting, setting clear terms in the policy to avoid situations inconsistent with the intent of classic and exotic car insurance. Policyholders who need broader usage flexibility may face distinct requirements or exclusions as outlined by insurers’ United States regulatory filings.

Vehicle owners in the United States considering coverage for a classic or exotic car are often encouraged to maintain extensive documentation, including ownership history, restoration expenses, and photographic evidence. This information may support both the underwriting process and any future claim submission. Insurers often include guidance on documentation requirements and may provide checklists to facilitate compliance with policy terms.

Secure storage and risk-reduction practices can play important roles in sustaining eligibility and premium levels for classic and exotic car policies. Insurers may specify garage requirements, alarm systems, or off-site storage options as preferable. Failure to meet these conditions might influence not only claims handling but ongoing coverage eligibility. Professional advice may be available through local collector car groups or insurance associations, although such information is not a substitute for direct carrier documentation.

Owners participating in exhibitions, rallies, or auctions may benefit from optional extensions or endorsements that address transit risks. These features are typically listed as separate items in policy documentation and may require additional premium contributions. Confirming coverage terms before vehicle movement or event entry is generally considered prudent to align with insurer expectations regarding risk exposures and coverage limits.

The development of classic and exotic car insurance in the United States continues to evolve as vehicle types, restoration techniques, and collector demographics change. Insurers may adapt eligibility criteria, broaden definitions of collectible vehicles, or refine risk-management requirements in response to market developments. Remaining attentive to policy updates and industry trends may assist owners in aligning insurance strategies with their specific needs.