Senior car insurance in Australia refers to vehicle insurance products designed for individuals in older age groups, often those aged 60 and above. This coverage may account for age-related changes such as reduced driving frequency, varied driving environments, and shifting personal needs. Multiple factors influence the way insurance providers structure policies for seniors, including regulatory requirements, coverage features, risk assessment methods, and typical claims history profiles.

Australian seniors evaluating their car insurance may encounter decisions involving policy types, included benefits, optional extras, and premium-setting criteria. Insurers commonly review the driver’s age, prior claims, vehicle characteristics, and regular usage patterns to determine policy costs and terms. Understanding these elements helps policyholders identify the cover options that suit their circumstances without relying on broad generalizations or specific endorsements.

Coverage options for seniors in Australia can vary based on the insurer’s risk models and available policy add-ons. Many providers allow policyholders to adjust excess levels, which can affect annual premiums and out-of-pocket costs per claim. Seniors may find that reducing annual mileage can sometimes be reflected in lower-priced options or restricted-use policies.

Driver history also plays a significant role. Insurance assessments may factor in recent claims, past traffic violations, and length of continuous driving experience. Providers may consider policyholders with accident-free records and long-standing licence tenure as lower risk, which could influence premium calculations.

Vehicle type and usage patterns are strongly considered. Seniors often drive smaller vehicles or late-model cars, which may attract lower premiums due to reduced repair or replacement costs. Declaring accurate information on how often and for what purposes the car is used supports compliance with policy terms.

Regulatory requirements in Australia set mandatory standards for motor vehicle coverage, such as Compulsory Third Party (CTP) insurance. All registered vehicles must carry CTP, but this does not protect against own-vehicle loss or additional third-party liabilities, so seniors often seek wider cover through comprehensive or third party fire and theft policies.

In summary, senior car insurance in Australia is shaped by the intersection of personal circumstances, vehicle details, policy features, and the national regulatory landscape. The next sections examine practical components and considerations in more detail.

Pricing for senior car insurance in Australia is determined by a range of variables rather than age alone. Insurers examine risk factors such as driving history, vehicle make and model, annual kilometres driven, and the insured postcode. While some insurers may offer tailored discounts recognizing limited or less frequent driving among seniors, each case is assessed individually to ensure compliance with regulations and actuarial standards.

The eligibility for particular insurance products does not depend solely on age, but also on other requirements such as holding a valid Australian driver’s licence. Some policies may specify upper age thresholds or request health declarations, especially if medical conditions are likely to affect safe driving. Insurers are obligated to comply with anti-discrimination regulations while maintaining prudent risk management practices.

Vehicle selection impacts pricing not only because of the car’s value, but also due to its safety features and repair costs. Seniors who opt for vehicles equipped with advanced driver-assist systems or features like automatic emergency braking may observe lower premiums, as these can reduce claims incidence or severity. Insurers may take into account how easily replacement parts are sourced and whether the vehicle is commonly targeted for theft in Australia.

Policy inclusions and exclusions can affect both the cost and scope of cover. Seniors may consider policies that include roadside assistance, new-for-old replacement, or safe driver initiatives. Such add-ons are factored into premium calculations, and the presence of optional covers often tailors the policy to the individual’s requirements. Reviewing the full Product Disclosure Statement (PDS) is recommended for clarity on benefits and any applicable restrictions.

Comprehensive car insurance remains a widely chosen option for seniors who wish to balance broad protection with flexibility in choosing additional benefits. This type of policy typically covers own-vehicle damage, third-party liabilities, theft, vandalism, and natural disasters. Some providers design policies specifically for older drivers, sometimes including optional add-ons aligned with typical usage patterns, such as reduced average annual mileage.

Third party property insurance is an alternative for seniors seeking to fulfil legal requirements and protect against the financial impact of causing damage to others’ vehicles or property. This form of cover is often selected when the insured vehicle is of lower market value, or when the cost of comprehensive insurance may not be justified by the car’s replacement value. Add-ons for fire and theft can be included based on individual needs.

Usage-based policies, also known as pay-as-you-drive or restricted-use policies, have become increasingly available in Australia. Seniors who drive infrequently may find that these policies take into account stated distance limits, with premiums calculated on expected annual kilometres. Such options often require periodic reporting or telematics devices to ensure the coverage remains matched to actual risk exposure.

Policy add-ons relevant for seniors include roadside assistance, windscreen and glass cover, and protection for personal belongings within the vehicle. These optional extras may incur additional premiums, but can provide reassurance and practical benefits for those travelling shorter or less predictable journeys. Seniors are encouraged to review whether these features are automatically included or available for selection when comparing coverage options.

All drivers in Australia, regardless of age, must maintain Compulsory Third Party (CTP) insurance. This is a mandatory minimum that covers injury to other people in the event of a crash but does not extend to vehicle damage. Insurers providing CTP cover are regulated at the state or territory level, with premium rates subject to oversight by authorities such as the State Insurance Regulatory Authority (SIRA) in New South Wales or the Motor Accident Insurance Commission (MAIC) in Queensland.

Anti-discrimination laws in Australia prohibit insurance providers from declining cover solely based on age. However, statutory exceptions may allow age-related risk factors to be considered when based on actuarial data or reliable statistics. If additional health declarations are required, these must comply with privacy requirements and cannot be used to impose unfair restrictions. Seniors can request access to any data used to make underwriting decisions as prescribed by the Disability Discrimination Act 1992 (Cth).

Insurance terms, including policy excesses, benefit limits, and claim processes, are closely regulated. Product Disclosure Statements (PDS) are legal documents providing information on features, exclusions, and obligations. Seniors are encouraged to refer to these to ensure full understanding of policy terms. The Australian Securities and Investments Commission (ASIC Moneysmart) provides consumer guidance on interpreting these documents.

Dispute resolution for senior car insurance in Australia falls under the remit of the Australian Financial Complaints Authority (AFCA). Seniors who experience issues with claims processing, premium changes, or policy cancellations have the option to seek a review via this authority, supporting transparency and consumer protections.

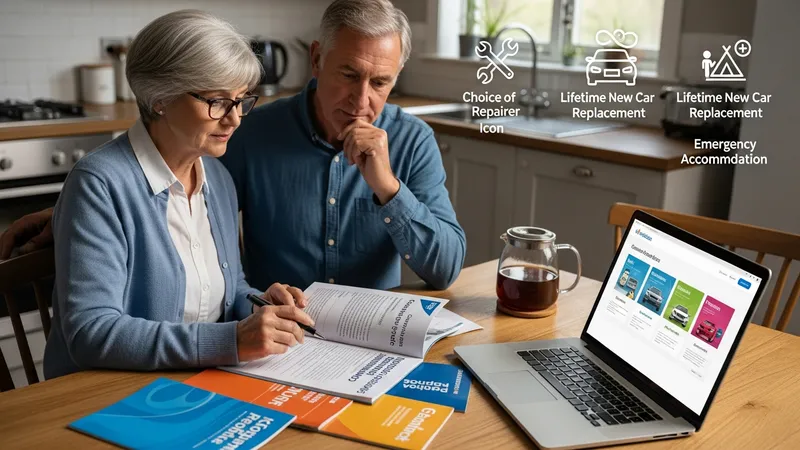

When comparing car insurance products, seniors in Australia may take several factors into account beyond just premium pricing. Particular attention is paid to the scope of coverage, including benefits such as choice of repairer, lifetime new car replacement, and emergency accommodation or transport. Annual policy costs can differ depending on included add-ons, declared vehicle use, and risk rating systems applied by the insurer.

Excess levels influence both upfront costs and post-claim expenses. Higher excesses may reduce annual premiums, but seniors need to consider outlay at claim time. The suitability of an excess level can depend on the policyholder’s financial position, frequency of claim history, and perceived risk tolerance. Some insurers may offer flexible excess options or waive excess under specific conditions, noted clearly in the PDS.

Customer service factors, such as claims processing speed, availability of helplines, and online management portals, commonly influence policyholder satisfaction. Australian seniors may value accessible communication options and clear support documentation, especially if managing policies for multiple vehicles or updating personal details.

It is typical for seniors to periodically review their car insurance agreements as circumstances change, including adjustments in driving habits, acquisition of new vehicles, or shifts in family arrangements. Many industry observers note a trend towards bundled home and car insurance due to the convenience and potential for streamlined administration, though price savings are not always guaranteed. Regular assessment enables alignment between personal needs and current cover options.