Digital wallets, often referred to as e-wallets, are software applications that facilitate the management of electronic financial transactions on digital devices. Within the context of Mexico, these fintech platforms enable users to conduct payments, transfer funds, and track financial activities without physically using cash or cards. These digital intermediaries typically connect to bank accounts, credit cards, or prepaid funds, creating a centralized space to handle financial operations. This form of payment management can integrate with various services, such as retail payments, utility bill settlements, and peer-to-peer transfers.

In Mexico, the rise of digital wallets corresponds with broader fintech developments fostering financial inclusion and modernization of payment ecosystems. Mexican e-wallets may employ regulatory frameworks established by national authorities, shaping the operational and security standards they observe. These wallets often utilize encryption and multifactor authentication to safeguard transactions and user data. Additionally, such platforms frequently support interoperability that aligns with Mexico’s banking infrastructure and newer instant payment schemes like CoDi (Cobro Digital), which may streamline fund transfers.

Mexican digital wallets typically vary in the scope of services offered, ranging from simple payment storage to more comprehensive financial management tools. Many e-wallets in Mexico allow users to connect with local banks and credit systems, enabling seamless fund movement within the national currency framework. Transaction fees may apply in certain circumstances, often depending on the type of transaction or the wallet provider’s fee structure set under Mexico’s regulatory guidelines. Users may also monitor transaction histories directly within the application for budgeting or record-keeping purposes.

Interoperability is an essential aspect of many Mexican e-wallet systems. Several platforms aim to facilitate payments not only at digital points of sale but also in traditional commercial establishments that accept electronic payments. Furthermore, as mobile device penetration in Mexico increases, digital wallets may extend access to users who previously relied primarily on cash, potentially contributing to shifts in consumer payment behavior. Payment tracking often features analytics or notifications to help users maintain visibility over their spending patterns.

The security aspect of digital wallets in Mexico is also guided by specific frameworks related to data privacy and electronic transaction security. Encryption methods, tokenization, and compliance with standards imposed by authorities like the National Banking and Securities Commission (CNBV) are common practices. Some Mexican wallets may integrate biometric authentication technologies, including fingerprint or facial recognition, to enhance access control. These security elements aim to reduce vulnerabilities and build user confidence within digital financial environments, although risks inherent to digital transactions may still require user awareness and precaution.

From an integration perspective, Mexican e-wallets may connect with various commercial and governmental payment channels. The adoption of the CoDi platform by Banco de México allows digital wallets to broaden payment acceptance across multiple sectors without relying on traditional card networks. The workflow within such wallets often includes steps for user identification, transaction authorization, and balance management, designed to suit both personal and business financial needs. As digital ecosystems evolve, Mexican fintech entities may continue adapting wallet features to fit emerging use cases and regulatory amendments.

As a summary, the digital wallets operating in Mexico function as electronic tools for managing money transfers, payments, and financial record-keeping. Their design incorporates technical, regulatory, and market considerations particular to the Mexican financial climate. The next sections examine practical components and considerations in more detail.

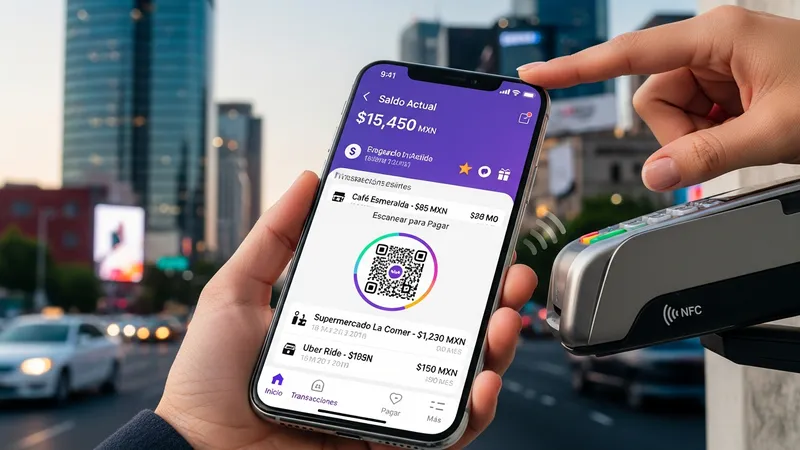

Digital wallets available in Mexico often include multiple functionalities beyond basic payment processing. Common features can include balance enquiry, transaction history logs, QR-code scanning capabilities for payments, and integration with loyalty or rewards systems. Many wallets also support bill payments directly from the app, providing a centralized platform for various financial duties. The extent of feature availability can vary depending on the issuing institution and regulatory permissions.

Some e-wallets in Mexico may incorporate contactless payment options through Near Field Communication (NFC) technology, allowing users to complete transactions at compatible terminals. This technology aligns with evolving consumer preferences for quick and convenient payment methods. Moreover, funds stored in e-wallets typically operate in Mexican pesos (MXN), conforming to local monetary regulations. Users may also link their e-wallet to Mexican bank accounts or prepaid instruments to facilitate fund loading and withdrawal operations within the national financial system.

Security features are often embedded within the functional design of Mexican e-wallet applications. These may include multifactor authentication, session timeouts, and real-time transaction alerts to enhance user oversight and protection. Additionally, some platforms implement artificial intelligence to detect potential fraudulent activities, although such systems may vary in effectiveness. The inclusion of these layers of control is frequently part of compliance with standards set forth by regulatory bodies like the CNBV.

From a user interface perspective, many Mexican digital wallets aim for accessibility on both smartphones and web platforms, enabling a broad range of users to interact with financial services regardless of device preference. The design focus often includes user-friendly navigation and clear transaction summaries intended to provide transparency and ease of use. However, the availability of advanced features may differ, depending on the wallet provider's technical capabilities and compliance adherence within the Mexican financial environment.

The operation of digital wallets in Mexico is subject to regulatory oversight primarily from the National Banking and Securities Commission (CNBV) and the Bank of Mexico (Banco de México). These authorities establish rules that fintech entities must follow to offer electronic payment services securely and transparently. Compliance requirements often include safeguarding user data, maintaining operational resilience, and ensuring transaction authenticity within the e-wallet environment.

Regulations may stipulate specific licensing for electronic payment institutions, mandating adherence to standards related to capital adequacy, risk management, and consumer protection. For instance, the Fintech Law (Ley para Regular las Instituciones de Tecnología Financiera) enacted in Mexico introduces a legal framework under which digital wallets must operate, highlighting transparency and anti-money laundering measures. These legal provisions aim to enhance trust and security in digital payment methods.

Security frameworks typically integrate cryptographic techniques such as TLS encryption for communication security and tokenization for safeguarding sensitive transaction data. Mexican digital wallets may also employ identity verification processes aligned with official identification systems like the CURP (Clave Única de Registro de Población). This can strengthen customer verification during account origination and transaction approval stages, potentially reducing fraud risks within the digital financial system.

Consumer protection under these regulations also requires clear disclosure of terms, fees, and dispute resolution procedures. Financial authorities in Mexico may promote educational initiatives to encourage informed use of digital wallets, emphasizing risk awareness and data privacy considerations. Such policies contribute to shaping the operational environment in which fintech entities develop wallet solutions adapted to national standards and user needs.

Digital wallets in Mexico often connect with existing banking infrastructure to facilitate fund transfers and payment acceptance. Integration mechanisms may include partnerships with Banco de México-supported platforms like CoDi, which enables instant payments via QR codes. This allows wallets to process transactions in real time across multiple vendors and service providers without the need for traditional card networks.

Wallet solutions may also interface with clearinghouses and electronic funds transfer systems regulated within Mexico to enable interoperability between different financial institutions. This connectivity can support practical use cases such as payroll distribution, peer-to-peer payments, and utility bill settlements. The increasing use of smartphones and internet access in Mexico supports broad adoption of these integrated digital wallet functionalities.

Some digital wallets may offer APIs to enable merchants and developers to embed payment acceptance into e-commerce and mobile applications. This capacity allows for expanded use of digital wallets beyond individual consumers to include business transactional workflows. The design of these platforms typically accounts for local transaction volumes and compliance demands to align with Mexico's financial ecosystem.

Ongoing technological advancements might influence future integration possibilities, including contactless payment acceptance at physical retail points and real-time financial data synchronization. These developments occur within the context of regulatory updates and evolving user preferences in Mexico's digital financial market.

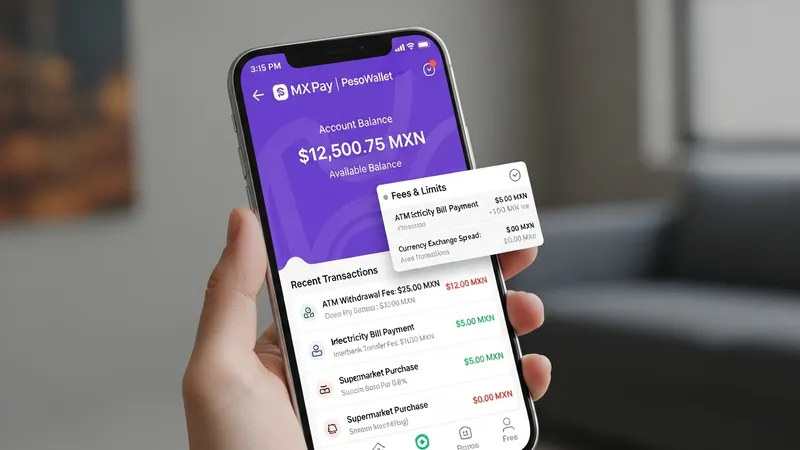

The pricing models for digital wallets in Mexico generally include transaction fees, account maintenance charges, or commissions on certain payment types. Fee structures often depend on the wallet provider's policies and regulatory limits established by Mexican financial authorities. For example, some wallets may apply charges for cash withdrawals or cross-institution transfers, while basic transactions could be free or incur minimal fees.

User considerations typically involve evaluating convenience against potential costs associated with wallet usage. Given that Mexican e-wallets are commonly denominated in Mexican pesos, exchange fees are usually not applicable for domestic transactions. However, cross-border transfers or currency conversions, if offered, may incur additional costs under prevailing local regulations.

Transparency in fee disclosure is often mandated under Mexican consumer protection rules, requiring digital wallet providers to present clear information regarding charges before users complete transactions. This practice aims to facilitate better user understanding and budgeting related to digital payment management. Additionally, the total cost of use may include indirect factors such as data usage for mobile applications or device compatibility requirements.

Finally, users may weigh security features, ease of access, and service coverage when selecting a digital wallet, balancing financial and functional attributes within the Mexican market context. These considerations align with the broader trend toward digital financial inclusion and the modernization of payment ecosystems.