Managing an investment portfolio with attention to tax outcomes involves arranging accounts, security types, and transaction timing so that taxes take a smaller share of long‑term returns. The concept centers on recognizing how federal tax rules affect dividends, interest, short‑ and long‑term capital gains, and distributions, then choosing accounts and instruments that align with those rules. This approach often considers retirement accounts, tax‑exempt instruments, and taxable brokerage accounts together rather than separately, because the placement of assets and the holding period for positions can materially influence after‑tax outcomes.

Key aspects include selecting the appropriate vehicle for each asset class, using holding periods to qualify for preferential capital gains rates, and applying loss recognition rules in a way that offsets realized gains when appropriate. In the United States, taxpayers commonly reference IRS rules on retirement accounts, capital gains, and wash‑sale adjustments when planning. These regulatory anchors define what is allowable and what administrative steps (reporting, basis tracking) typically accompany tax‑aware choices.

Asset location is a principal framework in this area: placing tax‑inefficient assets (taxable interest, actively traded bond funds) inside tax‑deferred or tax‑exempt accounts while holding tax‑efficient equity exposures (index funds, ETFs) in taxable accounts may often reduce annual taxable events. This placement strategy typically recognizes that bonds produce ordinary income taxed at federal rates, whereas qualified dividends and long‑term capital gains may receive preferential rates. United States taxpayers often compare the marginal federal tax treatment across account types to decide placement, while also accounting for state tax implications where relevant.

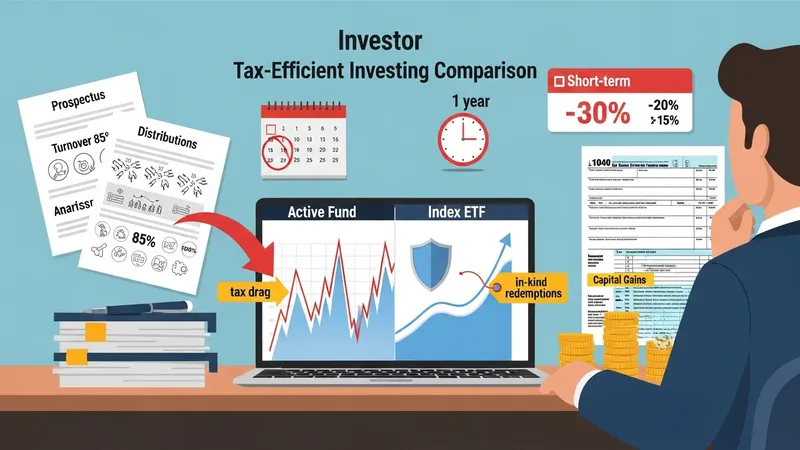

Holding period decisions affect whether a sale results in short‑term or long‑term capital gains. In the U.S., many taxpayers may qualify for reduced federal rates on long‑term capital gains and qualified dividends if a position is held beyond one year; therefore, turnover and trade frequency can create “tax drag” by converting potential long‑term gains into short‑term income. Tax‑aware managers frequently measure turnover and consider tax implications when evaluating active strategies, while noting that investor circumstances and tax brackets can alter the numerical impact.

Tax‑loss harvesting is an often‑discussed tactic that involves realizing losses in taxable accounts to offset realized gains or up to a specified amount of ordinary income per year, with excess losses carried forward. Application in the United States requires careful attention to the wash‑sale rule, which may disallow a loss if the same or substantially identical security is repurchased within 30 days. Publication 550 and IRS guidance outline these constraints, and investors may use diversified replacements or ETFs to maintain market exposure while attempting to preserve tax loss benefits.

Municipal bonds and municipal bond funds are frequently used for tax reduction in taxable accounts because interest from certain municipal securities may be exempt from federal income tax and, in some cases, state tax for residents of the issuing state. However, after‑tax yield comparisons and credit risk need to be weighed carefully: tax exemption does not eliminate credit risk or market risk. Investors commonly compare taxable equivalent yields and consult FINRA or other neutral sources for tax‑exempt bond characteristics.

Tradeoffs exist between deferring tax in retirement accounts and realizing tax‑free growth in Roth vehicles; for some U.S. taxpayers, converting assets into Roth accounts via conversions or contributing to Roth options may reduce taxes in later years but can generate current tax liability. These decisions typically depend on expected future tax rates, distribution timing, and individual circumstances. The next sections examine practical components and considerations in more detail.

Choosing which assets to hold in taxable, tax‑deferred, or tax‑exempt accounts is a foundational element in reducing tax drag. In the United States, typical account types include traditional IRAs and 401(k)s (tax‑deferred), Roth IRAs and Roth 401(k)s (after‑tax, potentially tax‑free distributions), Health Savings Accounts (tax‑advantaged for qualified medical expenses), and taxable brokerage accounts. Each account category has distinct tax treatment for contributions, growth, and distributions, and these differences often guide where investors place interest‑generating assets versus equity exposures. Considerations may include anticipated holding horizon and expected turnover.

Asset categorization often follows broad principles: tax‑inefficient assets that generate ordinary income are frequently held in tax‑deferred accounts, while assets likely to produce long‑term capital gains or qualified dividends may be placed in taxable accounts. For example, actively managed bond funds that distribute interest may typically create more annual taxable income than broad equity index funds, which may be more tax efficient when held in a taxable account. Information from the IRS on retirement plans and from FINRA on bond characteristics can help illustrate these differences for U.S. investors.

Employer plans such as 401(k)s may permit both traditional and Roth contributions, which introduces a planning consideration about current versus future taxation. In some U.S. cases, employees may find that pre‑tax contributions reduce taxable income now but shift tax exposure to retirement distribution years. Roth accounts shift that timing, so choosing between account types may involve comparing present marginal tax rates with expectations about future tax circumstances. These are considerations rather than universal rules, and they often motivate a mixed‑account approach.

Administrative practicality matters: tracking cost basis, wash‑sale impacts, and distribution timing often falls to the account holder or custodian. Tax reporting requirements for taxable accounts (Forms 1099, basis reporting) and for retirement distributions (Forms 1099‑R) are specific under U.S. tax law and may influence how smoothly certain strategies function. Many investors and advisors view reliable recordkeeping and software capable of tagging lots and tracking holding periods as an operational consideration when implementing tax‑aware placement choices.

Holding period rules determine whether gains are treated as short‑term or long‑term for federal income tax purposes, which can substantially change tax rates applied to realized gains. In the United States, holding an asset for more than one year often may qualify a gain for long‑term capital gains treatment, which for many taxpayers may correspond to lower federal rates than short‑term rates. Consequently, high turnover in a taxable account can increase annual realized taxable events and thereby produce greater tax drag compared with a lower‑turnover approach.

Quantifying the impact of turnover typically involves estimating pre‑tax returns and then applying expected tax treatments to realized income and gains. For widely held U.S. equity index funds or ETFs, lower realized distributions and in‑kind redemption mechanics may often translate into fewer taxable events. Conversely, actively traded funds or strategies that harvest gains frequently may realize more short‑term gains. Investors commonly review historical distribution patterns and turnover statistics, as reported in fund documents, to assess likely tax consequences before allocation.

The timing of sales relative to holding periods can also influence whether dividends qualify as “qualified dividends” under U.S. tax rules, which may receive preferential rates when the underlying holding meets certain holding period tests. For funds, the fund sponsor’s distribution regime and qualified dividend reporting can influence an investor’s after‑tax outcome. Therefore, understanding a fund’s historical classification of distributions and turnover may be useful as part of a tax‑aware evaluation.

Compliance with tax rules such as the wash‑sale provision is essential when attempting to realize tax losses. The wash‑sale rule may disallow a loss if the same or substantially identical security is repurchased within a 30‑day window, and publication 550 provides guidance on these mechanics. As a result, investors may consider how replacement securities affect portfolio risk while still aiming to preserve tax benefits; this operational tradeoff is an important consideration in implementation.

Selection of instruments in taxable accounts often focuses on products that historically generate fewer taxable distributions. In the U.S., ETFs and index funds are frequently cited for lower turnover and in‑kind redemption features that can reduce capital gains distributions, while actively managed mutual funds often have higher turnover and may distribute gains more frequently. The SEC provides general information on ETFs and mutual funds that may help investors compare structural differences that pertain to tax outcomes.

Municipal bonds and municipal bond funds are commonly considered in taxable portfolios because interest from certain municipal securities may be exempt from federal income tax and, in some cases, state tax for residents of the issuing jurisdiction. Evaluating tax‑exempt instruments typically involves comparing taxable equivalent yields and assessing credit quality and duration risk. FINRA and other neutral sources offer resources explaining the characteristics and risks of municipal securities for U.S. investors.

Tax‑managed mutual funds and ETFs aim to explicitly reduce taxable distributions through trading rules and realization management; however, their historical performance and tax outcomes vary by manager and market conditions. Reviewing fund prospectuses and tax information statements that report historical capital gains distributions helps demonstrate how a specific fund handled taxable events in prior years. These documents may illustrate patterns that investors factor into allocation decisions.

Dividend treatment is another consideration: qualified dividends may be taxed preferentially under U.S. rules if holding period and other requirements are met, while non‑qualified dividends are taxed as ordinary income. Fund and security selection that takes dividend characterization into account may change the expected annual tax footprint. Clear documentation and careful review of fund yield composition often form part of a tax‑aware selection process.

Beyond placement and selection, strategies such as Roth conversions, charitable donations of appreciated securities, and like‑kind exchanges for real estate can influence tax timing and eventual estate outcomes. Roth conversions may trigger current taxable income in exchange for potential future tax‑free withdrawals, and donating appreciated securities to eligible charities may allow a donor to avoid recognizing capital gains while claiming a charitable deduction within IRS rules. The IRS provides guidance on charitable contributions and on like‑kind exchanges under Section 1031 for qualifying real estate transactions.

Recordkeeping and reporting obligations are practical considerations: taxable accounts require accurate cost‑basis reporting (Form 1099‑B) and retirement accounts involve distribution reporting (Form 1099‑R). The ability to reconstruct lot‑level basis, holding periods, and the sequence of transactions may affect year‑end tax reporting and the capacity to substantiate claimed losses or gains. Taxpayers often view maintaining detailed trade records or using custodian reports as a preventive measure against reporting errors.

Legislative and regulatory changes can alter the effectiveness of particular techniques, so reliance on current U.S. tax law and published IRS guidance often informs any implementation. For example, preferential capital gains rates, limitations on itemized deductions, or modifications to retirement account rules may affect projected outcomes; therefore, many investors treat tax‑efficient methods as adaptable frameworks rather than fixed prescriptions. Monitoring authoritative sources is a part of maintaining alignment with evolving rules.

Implementing tax‑aware practices typically balances tax considerations with investment objectives, risk tolerance, and liquidity needs. While tax drag is an important factor, decisions may also reflect diversification, rebalancing, and income requirements. Understanding tradeoffs and documenting rationale under prevailing U.S. tax guidance may help investors integrate tax efficiency into broader portfolio management without treating tax minimization as the sole driver of allocation choices.