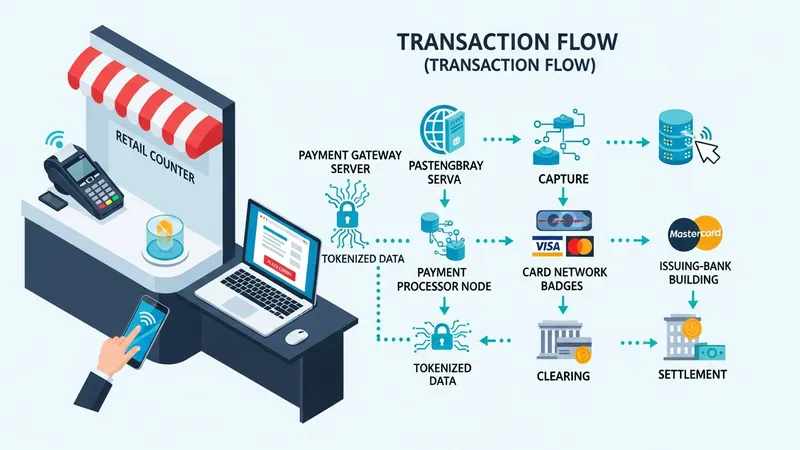

Credit card processing for businesses refers to the set of systems and agreements that enable a merchant to accept payment cards and receive funds. In the United States this typically involves a payment gateway that transmits transaction data, a payment processor that routes that data through card networks (such as Visa and Mastercard), an acquiring bank or merchant account that holds settlement funds, and the issuing bank that authorizes the consumer’s card. Each step—authorization, capture, clearing, and settlement—follows technical and banking procedures that connect point-of-sale or e-commerce systems with financial institutions and card networks.

These components can operate in different configurations: a merchant might use an integrated gateway and processor, a separate third-party merchant account, or an aggregated account offered by a payments provider. Online transactions often rely on tokenization and gateways to reduce the merchant’s card-data exposure, while in-person sales use terminals or payment terminals that implement EMV and contactless standards. In the U.S., card network rules, acquirer underwriting, and bank relationships influence how a business is onboarded and how funds are routed and settled.

Gateways and processors have distinct roles that often overlap in practice. A gateway primarily handles secure transmission of transaction data and may provide hosted payment pages, tokenization, recurring-billing tools, and developer APIs. A processor is responsible for routing transactions to the appropriate card network and handling settlement instructions between acquirers and issuers. In the United States, merchants often select an architecture based on integration needs, transaction volume, and acceptable levels of merchant account underwriting and operational responsibility.

Authorization and settlement involve multiple actors and timing considerations. Authorization is an immediate check with the issuing bank to confirm available funds and fraud indicators; capture and clearing follow once goods or services are provided, and settlement moves funds to the merchant’s acquiring account over one or more business days. Settlement timing can vary by acquirer and card type and often influences cash-flow planning for U.S. businesses, including any holds or reserve requirements imposed during onboarding.

Security and data scope influence implementation choices. Tokenization, point-to-point encryption (P2PE), and hosted payment pages can reduce the amount of cardholder data stored by the merchant and may narrow the merchant’s scope under the PCI Data Security Standard. U.S. firms often reference guidance from the PCI Security Standards Council and card networks when designing integrations to limit compliance burdens while maintaining necessary fraud controls.

Risk management, underwriting, and chargeback handling are routine operational considerations. Acquirers perform underwriting that considers business model, average transaction value, and historical risk; high-chargeback sectors may encounter additional scrutiny or reserve requirements. Chargeback processes are governed by card network rules and typically involve dispute windows, representment steps, and fees that can affect net receipts and operational processes for merchants in the United States.

Integration options and reconciliation methods vary by business size and sales channel. Retail merchants frequently use integrated point-of-sale systems with terminal hardware and payment processors that provide consolidated settlement reports; e-commerce merchants often rely on API-based gateways and vaulting for stored payment methods. Financial reconciliation across gateway, processor, and bank statements typically requires matching authorizations, captures, and settled batches, a process that can be automated with reporting tools or accounting integrations.

In summary, credit card processing for U.S. businesses involves coordinated roles for gateways, processors, acquirers, and issuers, with choices shaped by security, integration, cost, and risk-management considerations. The next sections examine practical components and considerations in more detail.

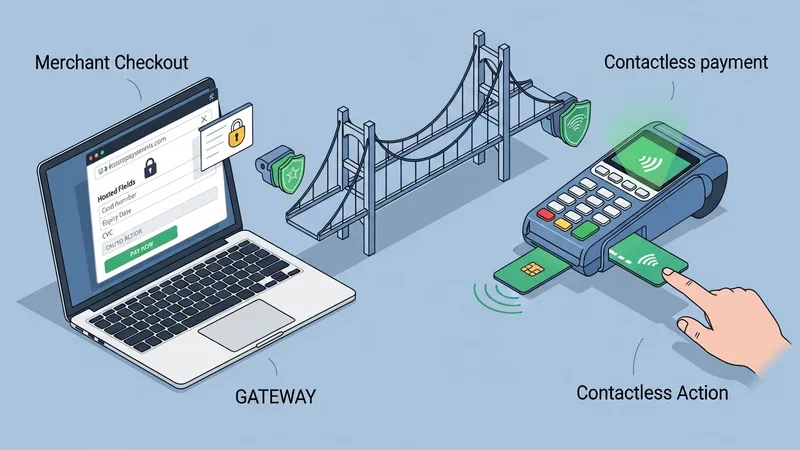

Payment gateways act as the technical bridge between a merchant’s checkout system and payment processors or acquirers. In the United States a gateway may provide hosted checkout pages, API endpoints for direct integration, tokenization services for stored credentials, and fraud screening tools. For online merchants, hosted pages and hosted fields can reduce the merchant’s handling of card data and therefore affect PCI compliance scope. For in-person commerce, gateways may also integrate with terminal hardware that supports EMV and contactless payments.

The authorization flow typically starts when a consumer submits card details: the gateway encrypts or tokenizes data, forwards it to a processor or acquirer, and receives an authorization response from the issuing bank. If approved, the merchant can capture the funds; captures may be immediate or delayed for pre-authorized transactions. Gateways commonly provide detailed transaction logs and batch reporting that reconcile authorization IDs, captures, and settled batches against the merchant’s bank statement.

Gateway selection in the U.S. often reflects integration needs and volume. API-driven gateways may suit merchants with technical resources who require custom checkout flows or subscription billing, while hosted checkout options can reduce development and compliance overhead. Many gateways also offer developer documentation, SDKs, and sandbox environments that allow merchants to test payment flows without sending live card data to networks during development.

Operational considerations include latency, uptime, and support for U.S.-centric card products. Gateways may include built-in fraud filters tuned to U.S. transaction patterns or tokenization schemes that comply with card network requirements. Merchants typically evaluate how gateways present reporting for reconciliation, whether they support multiple payment methods (card brands, wallets), and what mechanisms exist for dispute notifications and webhook events used in automated order-management workflows.

Merchant accounts are relationships between a merchant and an acquiring bank or an acquiring entity that enable settlement of card transactions. In the U.S., acquirers such as bank-affiliated services or independent acquirers take on merchant underwriting, set settlement timing, and may require documentation to assess business risk. Some providers offer aggregated or sub-merchant models where smaller merchants share an aggregate merchant account, while larger merchants often use dedicated acquiring accounts tied to their business bank accounts.

Underwriting processes may review business registration, average ticket size, chargeback history, and product category. Depending on risk factors, an acquirer can set rolling reserves, delayed settlement periods, or additional monitoring—measures that can affect cash flow. These practices are standard in U.S. acquiring relationships and are intended to manage fraud and potential losses, and they typically vary by industry and payment volume rather than being uniform across all merchants.

Acquirers and merchant-service partners commonly integrate with point-of-sale systems, gateways, and back-office software. For example, many retail chains in the United States connect terminals from certified vendors to their acquirer’s processing platform to obtain consolidated deposits and reporting. Bank-affiliated merchant services and independent acquirers each provide different contractual models and reporting interfaces that merchants may compare based on compatibility with their accounting and POS systems.

Settlement and reconciliation are central to the banking relationship. Acquirers aggregate daily batches of authorized transactions and initiate settlement to the merchant’s designated bank account after deducting interchange and any agreed fees. The timing and frequency of deposits can vary; merchants often coordinate with their accounting teams to map processor reports to bank deposits and to track chargebacks or adjustments that reduce settled amounts.

Security and regulatory compliance are core to card processing operations. The Payment Card Industry Data Security Standard (PCI DSS) outlines technical and operational requirements for entities that store, process, or transmit cardholder data; many U.S. merchants rely on measures such as tokenization, encryption, and hosted payment solutions to limit PCI scope. Additionally, EMV adoption for card-present transactions and support for contactless payments are widely implemented across U.S. terminals to reduce counterfeit fraud.

Tokenization replaces card numbers with non-sensitive tokens that can be used for recurring billing or card-on-file scenarios without exposing the primary account number. Point-to-point encryption (P2PE) can encrypt card data at the terminal before it reaches the gateway or processor. These techniques are often part of a broader security strategy that includes regular vulnerability assessments and adherence to card network technical guidelines published by Visa and Mastercard and referenced by the PCI Security Standards Council.

Chargeback management follows card network procedures and timelines that U.S. merchants must observe. When a consumer disputes a transaction, the issuing bank may initiate a chargeback; merchants receive notification and a timeframe to respond with evidence. Representment, evidence submission, and escalation steps are governed by network rules. Effective dispute handling often requires maintaining clear receipts, delivery confirmations, or digital transaction records that demonstrate fulfillment or authorization.

Regulatory and consumer-protection considerations can also affect processing practices. For example, the Federal Trade Commission (FTC) provides guidance on fair billing and consumer communication, and card networks publish operating rules that influence dispute resolution and fee assessment. Merchants typically align their policies and documentation with these frameworks to reduce exposure and to maintain consistent operational controls.

Costs in card processing are composed of several elements: interchange fees set by card networks and issuing banks, acquirer or processor markups, gateway subscription fees, per-transaction fees, and hardware expenses for terminals and point-of-sale systems. Interchange generally represents the largest single component and varies by card brand, card type (credit, debit, rewards), and transaction method (card-present, card-not-present). Processor markups and gateway fees are additional and are typically described in contractual statements provided by the acquiring party.

Typical U.S. pricing patterns can include monthly gateway fees in the range of about $10 to $30 for small merchants and per-transaction access or processing fees that may be a few cents to several tenths of a dollar plus a percentage of the transaction. Hardware for EMV-capable terminals can range roughly from $100 to $800 depending on features and whether the device supports contactless or integrated POS functions. These figures are approximate and may vary by provider and merchant profile.

Accounting for card processing requires reconciling gateway and processor reports with bank deposits. Merchants often map batches of settled transactions to daily or multi-day deposits, deducting interchange and processor fees shown as separate line items. Chargebacks and adjustments should be tracked as liabilities until resolved, and practices such as bookkeeping categorizations for fees, refunds, and chargebacks can aid in cash-flow forecasting and profit analysis for U.S. operations.

When evaluating cost structures, merchants in the United States commonly consider transaction volume, average ticket size, and the mix of card-present versus card-not-present sales. Higher volumes may support negotiation of pricing tiers or access to different contractual models with acquirers, while merchants with recurring billing needs may prioritize gateways that support tokenization and detailed reporting to automate reconciliation. These are considerations rather than guarantees, and outcomes typically vary by business profile and contractual terms.