Securing funding for a factory-built residence requires coordinated planning across budgeting, documentation, and lender interactions. The process typically involves estimating total project costs, assembling income and credit records, and understanding the sequence in which lenders review construction and purchase elements. Lenders may treat factory-built units differently from site-built homes depending on how they classify the structure and the collateral type, which can affect required documentation and underwriting steps. This overview explains the practical components commonly involved in preparing a budget and an application for financing such a residence, using neutral, descriptive language.

After initial cost estimation, prospective borrowers often gather proof of income, identity verification, and statements that show existing liabilities. Credit history and debt ratios are commonly assessed alongside documented sources of funds for down payments and contingency reserves. Timelines for approval may vary according to lender type, loan product structure, and whether the project includes new construction on a prepared site. The following examples illustrate tools and methods frequently referenced when organizing budget and application materials for factory-built housing projects.

When comparing lender expectations, applicants often find differences in documentation depth and underwriting triggers. Some lenders may require several years of tax returns and detailed contractor or manufacturer contracts that specify materials, timelines, and warranties. Others may focus primarily on credit history and current cash reserves. Understanding these variations can help organize a comprehensive file that typically contains identification, sequential income records, and project contracts or purchase agreements. It is informative to request a checklist from potential lenders early to align the application package with their documentation preferences and review procedures.

Itemizing the budget generally begins with the manufacturer’s base price and expands to include add-ons and selections that alter the final cost. Site-related expenses such as excavation, foundation, local permitting, utility connections, and delivery are often separate line items and can be significant relative to the unit price. Contingency funds are commonly recommended as a percentage of total estimated costs to accommodate unforeseen site conditions or schedule changes. Estimators may frequently suggest setting aside a contingency equal to several percent of the subtotal, though the precise amount can vary by project complexity.

Credit-related factors and debt-to-income measures frequently influence available loan terms and potential down payment expectations. Credit scores, recent late payments, and outstanding liens may be reviewed alongside current monthly debt obligations to determine capacity for new payments. Co-borrower arrangements or documented compensating factors such as sizable liquid reserves may be considered in underwriting evaluations. Because lenders use differing score thresholds and ratios, applicants often benefit from understanding the qualitative criteria that each lender highlights rather than assuming uniform requirements across institutions.

Scheduling and sequencing of application steps often combine lender milestones with manufacturer and site-preparation timelines. Typical phases include prequalification or preapproval, contract execution with the manufacturer, site preparation and permitting, and then final underwriting and closing. Inspection milestones and lien waivers may also form part of the process, especially when lender funds are disbursed over time. Maintaining clear, dated documents and regular communication between the manufacturer, site contractors, and the lender may reduce administrative delays and help keep the overall timeline coherent. The next sections examine practical components and considerations in more detail.

Income verification often begins with recent pay stubs, employer contact information, and signed tax returns covering one to two years where self-employment is involved. Lenders typically look for consistency in income streams and may request explanations for gaps or fluctuating earnings. Alternative documented income such as long-term rental receipts or retirement distributions is sometimes acceptable when properly substantiated. Credit evaluations commonly include score checks and tradeline reviews; recent derogatory marks can affect available loan structures. Organizing chronological, clearly labeled documents helps lenders follow income histories and can reduce back-and-forth during underwriting.

Debt-to-income (DTI) ratios are commonly used as a proxy for repayment capacity, with lenders calculating monthly debt obligations divided by gross monthly income. Exact thresholds may differ by loan type and lender, and presence of compensating factors—such as larger reserves—may be noted as context rather than a definitive remedy. Applicants sometimes include letters explaining non-recurring debts or one-time expenses to clarify ongoing capacity. Co-borrowers and co-signers change the profile lenders evaluate and may alter acceptable DTI calculations depending on each party’s documented income and liabilities.

Credit scores can influence not only approval likelihood but also the types of loan products a lender is willing to offer. Scores may affect underwriting overlays, required down payment percentages, and interest-rate differentials where applicable. Borrowers with limited credit histories sometimes use documented alternative credit sources, such as utility payment histories or rent payment records, that some lenders accept. It is informative to inquire with multiple lender types—bank, credit union, or specialist financiers—because each may apply different weight to credit and alternative documentation.

Verification processes may include automated income verification tools, manual review of originals or certified copies, and third-party employment verification. Turnaround times for these steps can vary; automated systems may return results in days while manual verifications can take weeks. Preparing clear, complete records in standardized formats—such as PDF bank statements and tax transcripts—tends to reduce clarifying requests. Applicants often find it useful to maintain a concise cover sheet that lists enclosed documents and identifies contact points for each item to assist the lender’s reviewer.

Estimating total project cost begins by separating the manufacturer’s unit price from site-specific expenses. Site work commonly includes clearing, grading, and foundation construction; these items are often contracted locally and priced independently of the unit. Utility connections for water, sewer, electrical, and septic can add material and labor costs that vary substantially with site accessibility. Transportation and crane or heavy-lift services for placing the modular sections are typical line items, and their costs may depend on distance, roadway access, and required permits. Collecting multiple estimates for site work often provides a more complete cost picture.

Options and interior selections from the manufacturer can incrementally increase the base price and may affect financing if they change the classification of the unit in terms of permanent attachment or system integration. External site upgrades, such as driveways, landscaping, and exterior finishes, are additional categories that can extend budgets. Professionals often recommend mapping each expense to a logical phase—purchase, site prep, set and hookup, final finishes—and documenting payment schedules to align with lender disbursement requirements. Clear phase delineation can assist both budgeting and lender review.

Contingency planning is a component of realistic budgeting, with commonly referenced contingency amounts often set as a percentage of the estimated subtotal to manage unforeseen conditions. The percentage may vary with site complexity, soil uncertainty, or supply-chain volatility; higher-risk scenarios may justify larger contingency reserves. Contingency funds can be held in a separate account or shown as available reserves in documentation to reassure underwriters evaluating project completion risk. Transparent documentation of how contingency funds will be accessed and used is typically useful during lender appraisal of project feasibility.

Permitting and inspection fees are frequently overlooked in initial estimates yet can affect timelines and cash flow. Local building departments may charge plan-review fees, permit fees, and inspection costs that vary by jurisdiction and project scope. Time required for permit approval can also influence when lender funds are needed, particularly if disbursements are tied to construction milestones. Including a schedule of anticipated permit steps and expected fee categories in the budget materials often clarifies the administrative and financial sequence for both applicants and lenders.

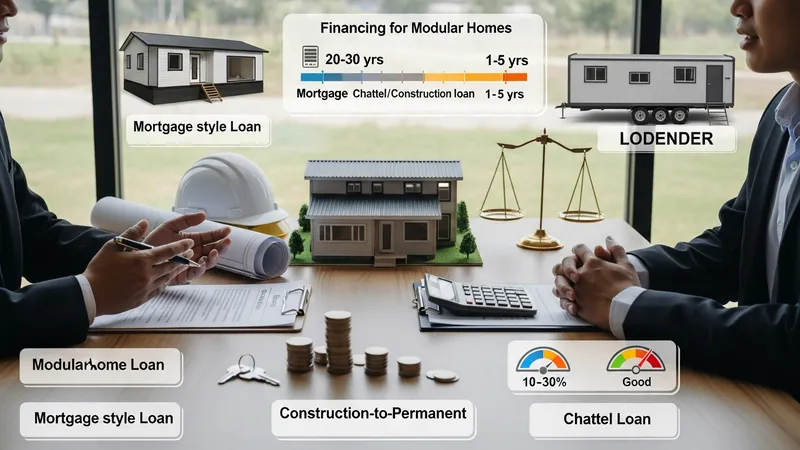

Financing approaches for factory-built units commonly include mortgage-style loans secured by the completed real property, construction-to-permanent loans that convert once the structure is installed, and personal property or chattel loans when the unit is not permanently affixed. Each approach may involve different underwriting standards, repayment terms, and collateral considerations. Term lengths for long-term financing often range from two decades to three decades where mortgage structures are used, while chattel or construction-only products frequently have shorter initial terms. Understanding the broad categories helps frame which documentation and timelines lenders will require.

Down payment expectations often vary by loan type and borrower profile; lenders may request higher initial payments where perceived project risk is greater. Typical down payment ranges are sometimes cited in percentage terms and may be influenced by credit position, loan-to-value calculations specific to the combined land-plus-unit value, and whether the borrower has substantial reserves. Interest rate levels and terms are sensitive to market conditions and borrower credit attributes; these influences are non-deterministic and change over time. Lenders may also include borrower escrow requirements for taxes and insurance where relevant.

Lender underwriting frequently considers the relationship between documented project costs and appraised value upon completion. Appraisals for factory-built units may involve comparative analysis of similar constructed properties or replacement-cost approaches depending on local appraisal practices. Where appraised value differs materially from the combined contract price and site improvements, lenders may request additional documentation, adjustments to loan sizing, or increased borrower equity. Clear, itemized contracts that tie unit specifications and installation responsibilities to firm prices can assist the appraisal and underwriting review.

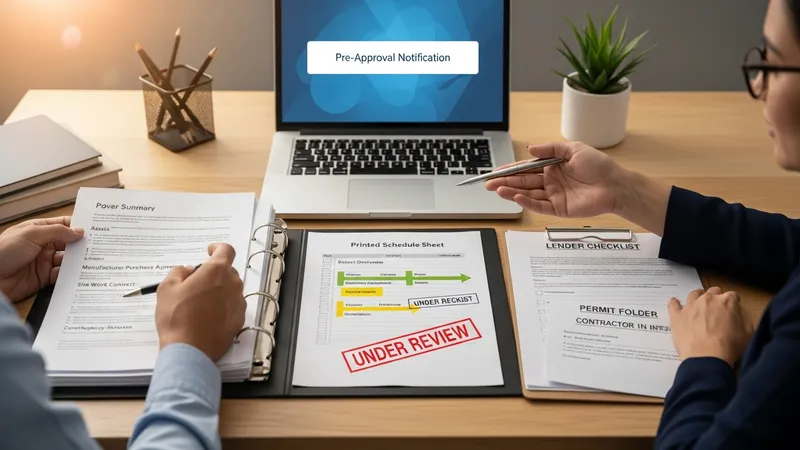

Qualification can also hinge on coordination among multiple parties: manufacturer, local contractor for site work, and the lending institution. Lenders often review manufacturer warranties, production timelines, and contractor qualifications as part of assessing project completion risk. Where funds are released in stages, lenders may require inspection reports or lien releases at each disbursement point. Applicants commonly benefit from documenting the sequence of responsibilities and agreed inspection triggers to explain how funds will be applied and how project milestones will be validated by independent parties.

Assembling a complete application package typically begins with personal identification, income verification, and current asset statements. Project-specific items commonly included are the manufacturer purchase agreement, a detailed site work contract, and a schedule that outlines delivery and installation milestones. Lender checklists may also request evidence of permits in process, letters of intent from contractors, and documentation of contingency reserves. Organizing these materials in a clear order and providing concise cover summaries can help underwriters navigate the file more efficiently and may reduce requests for clarification.

Prequalification or preapproval steps may occur early and offer an initial view of possible loan parameters based on submitted documentation. These preliminary assessments typically do not guarantee final terms but may indicate which loan product pathways are feasible. After contract execution, lenders often move into formal underwriting that verifies documents, orders appraisals or site inspections if required, and confirms title or lien status on the land. Turnaround times can vary widely; applicants should expect multiple weeks for underwriting in many cases, depending on the complexity and local administrative cycles.

Coordination between the lender, manufacturer, and local contractors is an operational consideration that frequently shapes the timeline. Delivery scheduling, required site readiness, and municipal inspection appointments can create dependencies that affect when funds must be available. When lenders disburse funds over a construction schedule, inspections or signed completion certificates may be required before each tranche. Clear communication protocols and an agreed schedule among the parties often help align funding releases with on-site work to minimize idle time and administrative hold-ups.

Final closing and occupancy steps commonly include verification that required inspections are complete, that any final municipal certificates are issued, and that title conditions are clear of unexpected liens. Lenders may require evidence of insurance coverage effective at closing and documentation confirming that permanent utilities are connected where needed. After closing, borrowers typically receive documentation that outlines repayment terms and any servicing contacts. Maintaining organized records of the entire project file supports future reference and may simplify routine loan servicing interactions.