Commodity trading activity in Hong Kong is organized around regulated exchanges, licensed intermediaries, and established clearing arrangements that support the negotiation and settlement of standardized agreements. Market activity typically covers derivatives such as futures and options, exchange-traded products that reference commodity prices, and a distinctive physical bullion market with historical local institutions. These elements together enable price discovery, risk transfer, and liquidity provision within a legal and operational framework centered in Hong Kong.

Trading in Hong Kong commonly uses electronic order books and defined contract specifications to reduce bilateral settlement risk and increase transparency. Supervisory oversight is provided by local regulators and exchange operators that set listing criteria, reporting standards, and participant rules. Market participants may include institutional traders, licensed brokers, commodity merchants, and a network of custodians and vault operators for physical delivery where applicable.

Contract standardization is a central feature that allows parties to trade without negotiating bespoke terms for each transaction. Standard contracts define lot size, delivery dates, tick sizes, and settlement methods; these factors can influence liquidity and the competitive participation of market makers. In Hong Kong, standardization may be supplemented by local conventions for physical delivery in certain markets such as bullion, where custody and assaying standards are part of the operational framework.

Regulatory oversight in Hong Kong may combine rules from the Securities and Futures Commission (SFC), exchange bylaws administered by HKEX, and membership rules from bodies such as the CGSE for physical bullion. These combined arrangements typically specify licensing for intermediaries, reporting and disclosure duties, and surveillance measures intended to limit market abuse. Market participants commonly review regulator notices and exchange circulars to remain aligned with compliance expectations.

Electronic trading infrastructure in Hong Kong is designed to support continuous order matching, pre-trade risk controls, and post-trade reporting. Market operators typically implement connection standards, co-location options, and market data feeds that facilitate price formation and arbitrage. For many commodity-linked ETPs and derivatives, real-time price feeds and clear contract specifications assist participants in monitoring exposures and implementing hedging strategies without needing direct bilateral negotiation for each trade.

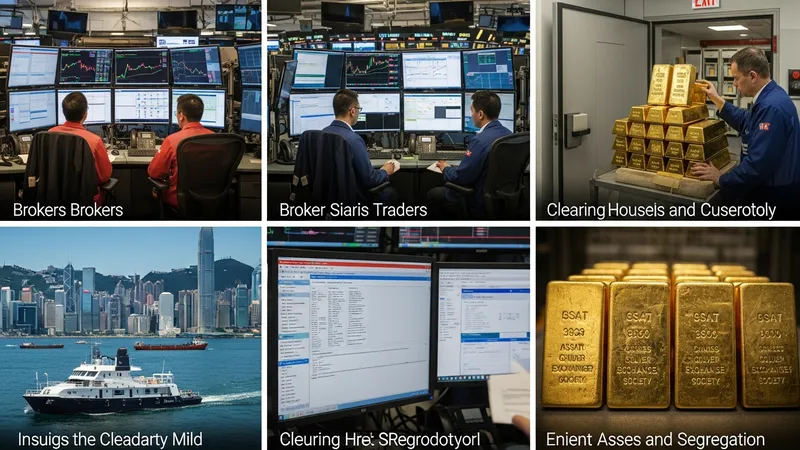

Clearing and settlement arrangements reduce counterparty exposure by centralizing trade novation through a clearing house. In Hong Kong, clearing houses linked to the main exchange assume the counterparty role after a trade is matched, with collateral and margining processes applied daily or intraday. These mechanisms commonly include variation margin, initial margin, and default procedures that can affect liquidity dynamics, especially during periods of heightened price movement.

In summary, Hong Kong’s commodity trading ecosystem typically combines exchange-traded derivatives, regulated ETPs, and an active physical bullion segment under coordinated oversight and standardized operational rules. These elements can support transparent price discovery and risk management for participants that engage through licensed brokers and custodians. The next sections examine practical components and considerations in more detail.

Participant roles in Hong Kong commonly include licensed brokers, proprietary trading firms, institutional investors, commodity merchants, vault operators, and clearing members. Licensed intermediaries operating in Hong Kong must typically comply with SFC regulatory requirements for conduct, client asset segregation, and reporting. Clearing members connected to HKEX’s clearing facilities usually meet capital and operational standards set by the exchange and relevant regulators, which can influence who is eligible to provide direct access to listed commodity contracts.

Regulatory responsibilities are distributed among local authorities and exchange entities. The Securities and Futures Commission often oversees market conduct and product authorisation, while HKEX enforces listing rules and market operation standards for exchange-traded derivatives. For physical bullion markets, membership organizations such as the Chinese Gold & Silver Exchange Society establish trading rules and local grading or assaying conventions. Market participants typically monitor guidance published on regulator and exchange websites for updates.

Compliance and reporting obligations may include trade reporting, position reporting, and periodic disclosure obligations for large exposures in certain contracts. These measures can support market transparency and assist surveillance. From a participant perspective, adherence to these regimes typically requires operational workflows for timely reporting, recordkeeping, and client communication. Firms often allocate dedicated compliance resources to track circulars from HKEX and notices from the SFC to maintain regulatory alignment.

Insider considerations for participants may involve membership selection, clearing connectivity, and the choice between direct clearing membership or accessing markets via broker custody arrangements. Firms considering direct membership often assess capital requirements, technology connectivity, and reconciliation processes. These considerations commonly affect cost structures and how firms manage operational risk within the Hong Kong commodity marketplace.

Electronic order matching and market data dissemination in Hong Kong are typically provided by exchange-operated platforms that support different product types, including listed derivatives and ETPs. HKEX operates trading systems that handle order entry, matching, and market data distribution; participants can subscribe to real-time feeds and access co-location services where available. Platform rules often include pre-trade risk checks to help limit the entry of orders that exceed predefined risk thresholds.

For exchange-traded products, issuer and distributor infrastructure intersects with exchange systems to ensure price transparency and secondary market liquidity. Market makers approved by exchanges or regulators may provide continuous two-sided quotes within specified parameters, which can support narrower spreads. Trading venues often publish circuit breaker rules, tick size tables, and trading session schedules that participants use to align their execution and monitoring processes in Hong Kong time zones.

Latency, connectivity, and data feed reliability are operational factors that participants commonly evaluate when selecting trading access options. Firms frequently choose between direct market access, sponsored access through brokers, or use of third-party trading platforms that aggregate liquidity. Technical considerations can affect execution quality and monitoring capacities; market participants often maintain contingency plans for system outages that reference exchange-mandated fault reporting procedures.

Transaction pricing structures may include per-trade fees, exchange levies, clearing fees, and market data charges. In Hong Kong, some of these fees are expressed as fixed HKD amounts per trade or as percentage-based levies assessed on transaction value. Participants typically incorporate these cost elements into execution planning and may compare cost profiles across product types to determine how pricing affects overall trading strategies.

Clearing in Hong Kong usually occurs through exchange-affiliated clearing houses that assume the counterparty role once trades are matched. These clearing houses implement margining frameworks designed to cover potential future exposure and Mark-to-Market variations. Initial margin levels and daily variation margin requirements are set based on risk models, historical volatility, and contract characteristics; market participants should expect these levels to be adjusted by the clearing house to reflect changing market conditions.

Default management procedures are formalised in clearing rules and commonly include auctioning or hedging of defaulted positions, application of default funds, and member assessment mechanisms. Such procedures aim to limit systemic impact by providing a structured sequence of actions in the event of member default. Clearing members typically maintain collateral in accepted forms and follow margin call processes that specify timelines for replenishment and enforcement.

Settlement for exchange-traded derivatives often involves cash settlement or physical delivery depending on the contract. For ETPs and physical bullion, settlement may involve securities settlement cycles and custody arrangements, including allocated versus unallocated storage distinctions for metal holdings. Custodians and vault operators in Hong Kong commonly follow documented chain-of-custody practices and insurance arrangements to support safekeeping of physical assets.

Risk management considerations include stress testing, daily reconciliation, and liquidity planning for margin obligations. Participants often model margin volatility and maintain liquidity buffers denominated in HKD to meet potential intraday or end-of-day calls. These practices can reduce operational stress in periods of market volatility and align participant procedures with clearing house expectations and local regulatory guidance.

Major commodity segments traded or referenced in Hong Kong markets include precious metals (notably gold and silver), commodity-linked exchange-traded products, and derivatives that reference international commodity benchmarks. Contract standards for listed instruments typically specify lot sizes, delivery months, tick sizes, and settlement methods. For precious metals, local practices may reference assaying standards and allocated vault storage arrangements governed by bodies like the CGSE and local custodians.

Price discovery in Hong Kong often depends on the interaction between local listed products and relevant international benchmarks. Exchange-traded instruments provide continuous intraday pricing that may reflect both regional demand and global commodity movements. Market liquidity and quoted spreads can vary across trading sessions, and participants commonly monitor both intraday order book depth and published reference prices issued by exchanges or approved pricing sources.

Contract design choices can influence market participation and usage. For example, smaller lot sizes and electronic accessibility tend to attract a broader set of participants, while larger contract sizes may primarily serve institutional hedgers. In Hong Kong, listing sponsors and product issuers collaborate with exchange and regulatory bodies to ensure contract terms are clear for market participants and that documentation reflects delivery, margining, and settlement conventions customary in the local market.

Operational considerations for those engaging with Hong Kong commodity markets commonly include understanding custody arrangements for physical delivery, reconciling position records with clearing members, and keeping abreast of exchange circulars that modify contract specifications or operational timetables. These practical elements shape how price signals are translated into executed trades and how market participants manage exposures within the established Hong Kong framework.